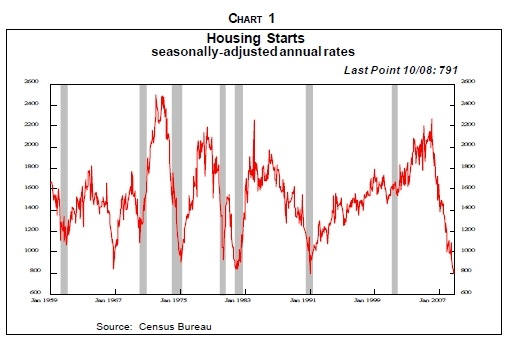

The housing market hasn't bottomed out yet.

For the third quarter, the closely-watched S&P Case-Shiller national

home-price index fell 16.6%, and experts are predicting further declines. Of

the top 100 markets, here are 10 with the worst forecasts.

Click here for more

Home values never went up.

By artificially

lowering the interest rates (Al Greenspan will go into history as the

bubble creator by excellence) they basically printed money and gave it

away to everyone. It was the ability to buy a higher loan that was

increased, not the VALUE of the property. No one's income went up, in

fact, because of the inflation, income came down.

According to a study of the Deutsche Bank by

2,011 half of the American home owners will be under water.The reason all this is important

is that, if you’re underwater, you’re much more likely to default on your

mortgage than if you have some equity.

Posted October 30, 2009

The worst U.S. housing crash since

the Great Depressionhas led to

a record number of foreclosures and shaved almost a third off property values.

The S&P/Case-Shiller Index of 20 cities in August was 29 percent below its 2006

high, after rising for four consecutive months...click

here for more...

Posted July 8, 2009 - Delinquencies

on U.S. Home-Equity loans reach record.

July 7 (Bloomberg) -- Late payments on home-equity

loans rose to a record in the first quarter as 18 straight months of job losses

and a slumping economy left more borrowers unable to pay their debts, the

American Bankers Associationreported.

Delinquencies on home-equity

loans climbed to 3.52 percent of all accounts from 3.03 percent in the fourth

quarter, and late payments on home-equity lines of credit climbed to a record

1.89 percent, the group reported today. An index of eight types of loans rose

for a fourth straight quarter, to 3.23 percent from 3.22 percent in October

through December, the group said.

Posted June 7, 2009 - Take some time

to watch this video clip!

Posted June 4, 2009

Posted May 12, 2009

The median U.S. home price

dropped 14% in the 1st quarter from a year earlier. The average median existing

home price declined to $ 169,000 and distressed properties sell typically for

20% less than other homes on the market.

Posted May 1st 2009

Foreclosures keep rising.

Those who even dare to hope we've seen the end of the real estate problems are

in for a huge surprise.

Home sales are not any better....

Posted February 23, 2009

New York

apartment prices are very high relative to the observable fundamentals.

Using

three alternative yardsticks-price/rent, price/income, and affordability-we find

that prices would need to decline by 35%-44% to return to the valuation

levels seen in the 1995-1999 period, before the start of the recent boom.

Under the

(admittedly unrealistic) assumption that prices decline by the same percentage

in each market segment, this type of drop would imply that a 1- bedroom condo

whose price currently averages roughly $800,000 would decline to $480,000; a

2-bedroom condo would decline from $1.7 million to $1 million; and a 3-bedroom

condo would decline from $3 million to $1.8 million.

As Manhattan

is firing more and more people, the odds are that incomes will fall back to the

pre-1986 level of 2 times the national average-and if national per capita income

remained unchanged-prices would need to fall as much as 58% to return to the

1995-1999 price/income ratio.

Posted February 5, 2009

The Real Estate slump isn't over yet.

Just like the Spanish banks, the American banks keep sitting on their

foreclosures so they can spread the pain...click

here for more...

Posted December 23,

2008

Sales prices for existing

U.S. homes fell the most on record in November, tearing a deeper hole into

households’ already tattered finances. The median resale price fell 13 percent

from a year before, to $181,300, “probably the largest price decline since the

Great Depression,” National Association of Realtors Chief Economist Lawrence Yun

said in Washington. Sales slid to an annual rate of 4.49 million, lower than

forecast.

New Home inventories are

soaring to unseen levels:

New-home sales tumbled 5.3% to the lowest level in 17 years

during October, while prices kept retreating.

Posted September 18 and

updated October 27,

2008

We start to see REAL

SALES. Asking prices are half of what they were only a couple of years ago.

Opportunities start to show! Foreign buyers are flocking into the USA and

Florida to buy Real Estate.

The number of homeowners

ensnared in the foreclosure crisis grew by more than 70 percent in the third

quarter of this year compared with the same period in 2007, according to data

released Thursday.

Nationwide, nearly 766,000

homes received at least one foreclosure-related notice from July through

September, up 71 percent from a year earlier, said foreclosure listing service RealtyTrac Inc.

Posted September 4,

2008

The decline in home prices hasn't

been seen since the Great Depression, Gross said. That drop translates to an

even bigger decline in overall wealth as the effects ripple through markets,

Gross said. Home prices in 20 of the largest U.S. metropolitan areas fell

15.9 percent in June from a year earlier, according to an S&P/Case-Shiller

index.

Posted August 5, 2008

Former Fed Chairman Alan Greenspan

orchestrated the Real Estate bubble and hereby enabled the American economy to

survive somewhat longer. Now that he has little political obligations left (does

he?) his comments have become more reliable.

Amazing is what he said last week: " The falling home prices in America are

"nowhere near the bottom" – you can take to the bank. This may

surprise some, especially since the national media just reported the

single largest year-over-year drop in U.S. home prices, May's record 15.8%

plunge.

Even worse is that according to realtors,

appraisers, homebuilders and mortgage brokers, the Home sellers still don't get

it! Home prices didn't soar for any sound fundamental reason. They soared

because of low interest rates,easy credit and a $500,000

capital gains tax exemption. (A misallocation of funds, in other words.)

Posted July 31, 2008

The American Real Estate market is in a

really bad shape. Prices are coming down, and so has the dollar. In other words,

we have ‘SALES’. More and more opportunities are seen, especially for the

European Investor.

Waiver: The information at

this site is provided solely for informational purposes and does not constitute

an offer to sell, rent, or advertise real estate. The owner is not making any

warranties or representations concerning any of these properties including their

availability. Information at this site is deemed reliable but not guaranteed and

should be independently verified. However, due to our experience, we are

in a position to advice the potential investor as to where and how he should

handle his planned American Real Estate investment(s), and how it can be rented

out and maintained.

Indicative prices for the properties below

range from $ 75.000/€ 50,000 to $ 250.000/€ 180,000

June home foreclosures up 53 percent Thu Jul 10, 2008 6:12am EDT

By Helen Chernikoff

NEW YORK (Reuters) -

Home foreclosure filings jumped 53 percent in June from a year earlier, although

they were down 3 percent from May, and foreclosures are expected to rise

further, real estate data firm RealtyTrac said on Thursday.

Foreclosure filings

rose on an annual basis in 39 states to a total of 252,363 properties during the

month, with Nevada, California, Arizona and Florida posting the highest

foreclosure rates.

One out of every 501

U.S. households received a notice of default, auction sale or bank repossession

in June, RealtyTrac said.

"June was the second

straight month with more than a quarter million properties nationwide receiving

foreclosure filings," said James J. Saccacio, chief executive officer of

RealtyTrac. "We have not yet reached the top of this foreclosure cycle."

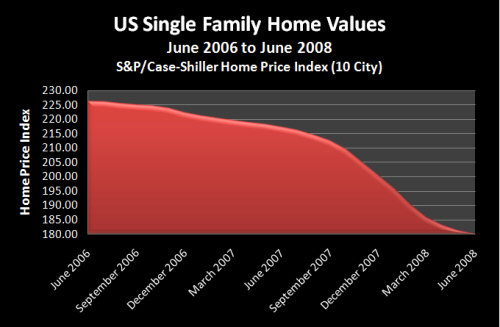

Record drop in US home prices - AP - Jun 24 2008 9:02PM

New

York - US home prices tumbled in April at the fastest rate since a widely

followed index was begun in 2000 with all 20 metropolitan areas surveyed

posting annual declines for the first time.

The Standard &

Poor's/Case-Shiller home price index of 20 cities fell by 15.3% in April

versus a year ago, according to Tuesday's report. Prices nationwide are at

levels not seen since August 2004. The narrower

10-city index declined 16.3% in April, its biggest decline in its more than

two-decade history.

Meanwhile, a report

from the Office of Federal Housing Enterprise Oversight said US home prices

fell 4.6% in April from the same month last year, when the index peaked.

That marked the biggest decline ever in the agency's monthly index which

dates back to January 1991. The government

index is calculated using mortgage loans of $417 000 or less.

While the

government report has shown nationwide price declines, the Case-Shiller

index has shown far greater drops because it focuses on larger cities where

prices rose further during the boom years, and includes riskier loans.

No surveyed city

stayed above water, according to the Case-Shiller index. The last holdout,

Charlotte, North Carolina, finally succumbed to the national housing

downturn, with prices there slipping 0.1 percent from a year ago. Las Vegas and Miami

both continue to post the largest declines, falling 26.8% and 26.7%,

respectively.

However, the annual

declines in Denver, Dallas and Cleveland were less severe than in the

previous month, but Maureen Maitland, a S&P vice president, is reluctant to

peg that as an indication of stabilization. "We wouldn't call a

trend on one-month data," she said.

The report also

showed prices in eight metro areas increased in April from March, but the

gains could be seasonal blips as the home-buying spring season starts up

rather than a sign of a turnaround, Maitland said. The housing slump,

along with higher food and fuel prices and disruptions in the credit

markets, has taken its toll on consumer sentiment.

An industry group

Tuesday said US consumer confidence fell unexpectedly sharply in June to the

fifth-lowest level ever. The Conference Board's reading of consumers'

expectations also hit an all-time low.

- AP

US housing crisis deepens as foreclosures soar- June 13, 2008

Foreclosures add to the Credit Crunch, the Crack-up boom, the destruction of

fiat money and will push up interest rates substantially in the near future. The

problem ain't going away as the vicious circle is closed!

By James Quinn, Wall

Street Correspondent

America's housing

crisis is reaching near-catastrophic levels as the number of people losing their

homes and those seriously behind on mortgage payments soared last month.

One in almost every 500 American mortgage holders now has either lost their home

or is on the verge of losing it, as the credit crisis claims victims throughout

the US.

US banks repossessed almost three times as many homes in May as they did in the

same month last year, taking control of 73,974 homes, against 28,548 in May

2007, according to a survey by RealtyTrac, the property research group.

The level of foreclosures - the legal process a bank begins to reclaim property

after a mortgage holder falls badly behind on payments - rose by 48pc last month,

the 29th consecutive month of year-on-year increases.

The states of Nevada,

California and Arizona are the biggest victims of the housing crash. In Nevada,

one in every 118 households received foreclosure notices in May. In Arizona, the

figure was one in every 201 households.

The current crisis was

sparked by an environment of low interest rates and lax lending practices among

many mortgage brokers. As a result, and despite the US Federal Reserve reducing

interest rates to 2pc from 5.5pc last September, a growing number of Americans

cannot afford to meet their mortgage payments as the US economy continues to

falter.

Inflation is adding to

their woes, with the US Consumer Price Index rising 0.6 percentage points in

May, up 4.2pc in the year, with core prices, stripping out fuel and food, up

0.2pc to 2.3pc.

U.S. Economy: Home Resales Decline, Inventories Jump (Update2)

By Shobhana Chandra –

Friday May 23, 2008

May 23 (Bloomberg) --

Sales of previously owned homes in the U.S. fell in April and the supply of

unsold properties reached a record, signaling no let-up in the 27-month housing

slump.

Purchases declined 1

percent to an annual rate of 4.89 million, higher than forecast, the National

Association of Realtors said today in Washington. The

median price fell 8 percent from April last year, the second-biggest drop.

``There is no

indication that things are improving,'' said

Christopher Low, chief economist at FTN Financial in New York, who forecast

sales would drop to a 4.9 million pace. ``Inventories will stay out of balance

at least until the end of 2009 and prices will keep falling.''

Defaults on subprime

mortgages have prompted lenders to restrict credit, while falling

property values have given buyers who are still able to get financing reason

to delay purchases. The slide in home values may hurt consumer spending, which

accounts for more than two-thirds of the economy.

Glut of Homes

The number of

previously owned

unsold homes on the market at the end of April jumped to 4.55 million from

4.12 million in March. The total represented 11.2 months' supply at the current

sales pace, the highest on record and up from 10 months at the end of the prior

month.

The

median price of an existing home fell to $202,300 from $219,900 in April

2007.

``We had an unrealistic

run-up of prices and the faster they come back down to the real world the

better,''

William Cheney, chief economist at John Hancock Financial Services in

Boston, said in an interview with Bloomberg Television. ``The faster prices come

down, the quicker we can get back to an equilibrium where we actually have

transactions.''

In Florida for a home purchased in

2006 at $350,000 the monthly payments are $3200 dollars at a 5% interest

rate. Renting it out earns $1200 dollars a month. The asset you purchased does

not pay for itself and in fact, it is the definition of insolvency--it consumes

more than it produces. Year over year the Case -Shiller home prices index

are down over 14%, declining at a 24% rate.